By Amjad Suri

India has ranked twelve out of 26 countries in the 2016 Brooking financial and digital inclusion project report(FDIP).The rankings show India dropped 3 places in FDIP report over last year’s 9 out of 21 countries.

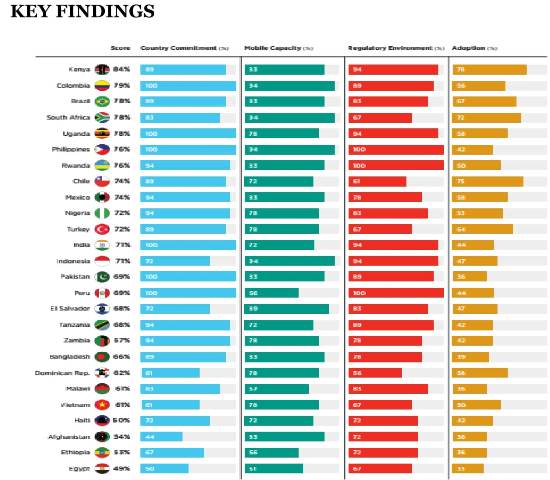

The Brookings FDIP report evaluated 26 countries that are economically, politically and geographically diverse with their respective descending score cards are Kenya (84%), Columbia (79%), Brazil, South Africa and Uganda (tied at 78%),Philippines and Rwanda (tied at 76%), Chile and Mexico (tied at 76%), Nigeria and turkey (tied at 72%),India and Indonesia (tied at 71%), Pakistan and Peru(tied at 69%), El Salvador and Tanzania (tied at 68%), Zambia(67%), Bangladesh (66%), Dominican Rep. (62%), Malawi and Vietnam (tied at 61%), Haiti(60%), Afghanistan (54%), Ethiopia (53%) and Egypt (49%).

The 2016 FDIP report evaluates and ranks countries based on four dimensions–country’s commitment on financial inclusion, its mobile capacity, the regulatory environment, and adoption of financial services. India’s overall score was 71 percent points, which was better than the last year score of 72 percent.

Country Commitment (100 percent) – PradhanMantri JanDhanYojana (PMJDY)

In its financial and digital inclusion project report(FDIP) 2016, Brookings said India’s commitment to financial inclusion scored 100 percent. This figure was achieved through implementation ofPradhanMantri Jan DhanYojana (PMJDY) program, launched in 2014. The program has demonstrated considerable impact with respect to expanding financial access, although dormancy rates indicate that efforts to promote financial capability and enhance the utility of financial products and services.By May 2016, PMJDY opened 200 million bank accounts and opened account of 100 percent of financially excluded.

India joined Better Than Cash Alliance and issued provisional payments bank licences to diverse entities, including non-bank institutions such as India post in 2015 were some of the exemplary achievements.

MobileCapacity(72 percent)-Cost effective measures to promote financially excluded groups

Mobile money has contributed to enhanced adoption of formal financial services in India, which scored 72 percent among the FDIP countries in terms of mobile money account ownership.Mobile capacity is based on unique mobile subscription,3G coverage, mobile money deployments,domestic transfer through websites and bill payment facilities.According to the world bank’s financial inclusion (Global findex), only 2 percent of adults in India had a mobile money account in 2015.

Increasing mobile network coverage by population and money offerings could boost India’s mobile capacity core in future.

Regulatory environment (94 percent)-Advancing regulatory efforts designed to facilitate financial inclusion

Strong regulatory provisions enable financial service providers to explore means of leveraging the proliferation of available consumer data to facilitate access to financial services among those who need them.TheRBI guidelines in 2014, asked non-bank operators such as mobile network providers to leverage their distribution expertise to advance financial access and use among underserved groups.

Finalizing the money transfer regulations in order to formalize KYC process and entry on non-bank mobile operators would boost the financial inclusion heavily.

Adoption (44 percent)- Facilitation is important

Adoption of digital financial services such as mobile money is minimal vis a vis traditional bank accounts.WhilePMJDY promote ownership of bank accounts but dormancy rates is high as 40 percent in the operating account according to the world bank’s financial inclusion (Global findex) in 2014.

Findings from a November 2015, USAID publication regarding digital payments in India highlighted low levels of awareness and adoption of digital financial services. For example, only about 30 percent of individuals who did not hold debit cards were aware of debit cards, and among those who did not use mobile money, only about 20 percent were aware of mobile money or e-wallets.

Way Ahead

While advancing access to formal financial services is a key priority of the government, financial inclusion authorities recognize that the quality of these services is critical to promoting financial health.

Over the coming months, payments banks must surmount logistical challenges involving the setup of subsidiaries and hiring staff, as well as determining a viable business model, in order to expand access to financial products and services among financially excluded communities.

Finally,government and private sector stakeholders must work together to address barriers to financial inclusion among women, migrants, and other underserved populations. Increasing adoption of digital financial services in particular could help drive financial inclusion among these groups.

****

(Amjad Suri is a UAE based financial consultant)